Kwasi Kwarteng’s first set piece as Chancellor of the Exchequer was never going to be easy, even before the 0.5% increase in interest rates the day before. The new Prime Minister Liz Truss revealed much of what we might expect before Mr Kwarteng spoke a word, so we already knew that there would be:

- a two-year £2,500 Energy Price Guarantee (EPG) for consumers;

- similar but shorter-lived support for businesses and other non-domestic energy users;

- cuts to National Insurance Contribution (NIC) rates; and

- a reversal of the planned April 2023 increases in the rate of corporation tax.

Nevertheless, Mr Kwarteng’s launch of ‘The Growth Plan’ contained some surprises, including the end of additional rate income tax (outside Scotland) and the reversal of recent changes to IR35.

Contents

- Economic Update

- Tax Announcements

- Other Announcements

- The energy price schemes

Economic Update

The Chancellor launched his Growth Plan against a challenging economic backdrop.

Inflation is currently running at an annual 9.9% and on Thursday 22 September, the Bank of England announced its seventh consecutive increase in bank rate to 2.25%. In its latest Monetary Policy Report, the Bank of England said that it expected inflation to peak in October 2022 at just under 11% and remain above 10% over the following few months before starting to fall back.

High inflation and rapidly rising interest rates are taking their toll on public finances. The latest estimates from the Office for National Statistics (ONS) show Government borrowing for August 2022 to be almost twice the figure projected by the Office for Budget Responsibility (OBR) six months ago. Total Government debt now amounts to £2,427.5 billion, equivalent to 96.6% of gross domestic product (GDP). Servicing costs on that debt pile, which have been driven upwards by the cost of servicing gilts linked to the retail prices index (RPI), could reach £100bn in 2022/23.

Ahead of the Chancellor’s statement, there was some discussion about the Bank of England and the Government pulling in opposite economic directions. The bank wants to slow the economy to subdue inflation predicting that the economy would shrink in the third quarter. That would be the second successive quarterly decline, meeting one common definition of a recession.

However, both 10 and 11 Downing Street are focused on economic growth as a way out of the UK’s long-lasting economic malaise, hence the ‘The Growth Plan’ branding of today’s statement and an extra £72.4 billion of Government borrowing in the current financial year.

Tax Announcements

Income tax

The reduction in the basic rate of income tax to 19%, which was originally scheduled for 6 April 2024, will now take effect from the beginning of the 2023/24 tax year.

A four-year transition period for gift aid relief will maintain the income tax basic rate relief at 20% until April 2027. A one-year transitional period for relief at source will allow pension schemes to continue claiming relief at 20%.

The additional rate tax of 45% that currently applies on annual income over £150,000 in England, Wales and Northern Ireland will be abolished from 2023/24.

These changes do not affect Scottish tax rates.

The additional rate for savings, dividends and the default rates will also be removed from April 2023 and this change will apply across the whole of the UK.

Dividend taxation

From 2023/24, the tax rates applicable to dividends will be reduced by 1.25 percentage points, taking them back to 2021/22 levels.

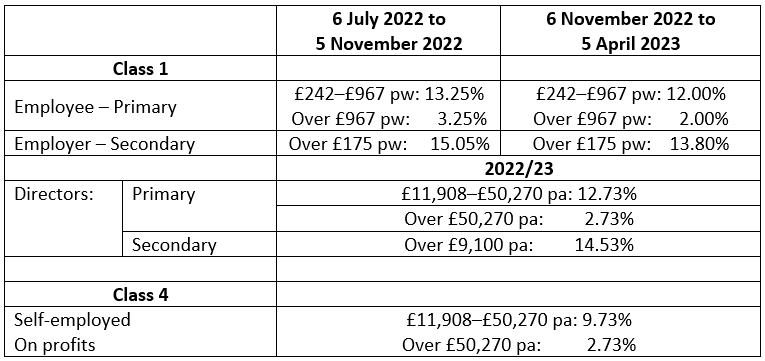

National Insurance Contributions

The additional 1.25 percentage points previously added to all 2022/23 Class 1 and Class 4 NIC rates will be scrapped. The change will take effect from 6 November 2022.

The 1.25% health and social care levy, due to replace the NICs increase from 2023/24, will be abandoned.

There is no change to the increased 2022/23 Class 1 primary threshold and Class 4 lower profits threshold announced in the Spring Statement 2022.

The rates and thresholds for the rest of the 2022/23 tax year for those affected are as follows:

IR35 – off-payroll working

The 2017 and 2021 reforms to the off-payroll working rules (commonly known as IR35), which required employers to categorise their workers, will be repealed from 6 April 2023.

From 2023/24, workers providing their services via an intermediary, such as a personal service company, will be responsible for determining their employment status and paying the appropriate amount of tax and NICs.

Stamp duty land tax

Stamp duty land tax (SDLT) rates for residential property will be revised from 23 September 2022, increasing the 0% band threshold from £125,000 to £250,000.

The Government will also increase relief for first-time buyers, raising the 0% band threshold from £300,000 to £425,000 and the maximum value of property on which they can claim the relief from £500,000 to £625,000.

These changes only affect England and Northern Ireland. The Scottish Government has announced that it will set out its plans for land and buildings transaction tax as part of the normal budget process and the Welsh Government has given no information about its land transaction tax.

Corporation tax

The increases to corporation tax rates due to take effect from April 2023 will no longer take place. The main rate of corporation tax will remain at 19%.

The corresponding increase in diverted profits tax from 25% to 31% will also be cancelled from April 2023.

Furthermore, the 5% reduction in the bank corporation tax surcharge will no longer take place, meaning it will remain at 8%.

Annual investment allowance

The current £1 million level of the annual investment allowance will be made permanent.

Capital allowance – super-deduction

Some of the technical provisions for the super-deduction will be amended to ensure that the relief continues to operate as intended, despite the cancellation of the corporation tax increase.

Company Share Option Plan

From April 2023, qualifying companies will be able to issue up to £60,000 of Company Share Option Plan (CSOP) options to employees, doubling the current limit. The ‘worth having’ restriction on share classes within the CSOP will be eased, better aligning the scheme rules with the rules in the Enterprise Management Incentive (EMI) scheme and widening access to CSOP for growth companies.

Venture capital schemes

From April 2023, companies will be able to raise up to £250,000 of seed enterprise investment scheme (SEIS) investment – a £100,000 increase on the current limit. At the same time:

- the gross asset limit will be increased to £350,000;

- the company age limit will be raised from two to three years; and

- the annual investor limit will double to £200,000.

The SEIS, enterprise investment scheme (EIS) and venture capital trust (VCT) scheme will now be extended beyond 2025.

Office of Tax Simplification

The Office of Tax Simplification (OTS) will be abolished, to be replaced with a mandate to the Treasury and HMRC to focus on simplifying the tax code.

Other Announcements

Investment zones

The Government will work with the devolved administrations and local partners to introduce investment zones across the UK. These zones will have a range of benefits, including:

- time-limited tax incentives;

- accelerated development with streamlined planning requirements; and

- greater control over local growth funding for areas with appropriate governance.

The following are among the ten-year tax-incentives that are being considered for England:

- 100% relief from business rates on newly occupied business premises and certain existing businesses where they expand into an English investment zone tax site;

- 100% first-year capital allowances for plant and machinery;

- accelerated relief to allow businesses to reduce their taxable profits by 20% of the cost of qualifying non-residential investment a year;

- zero-rate employer NICs on salaries of any new employee working in the tax site for at least 60% of their time, on annual earnings up to £50,270; and

- full SDLT relief for land and buildings bought for use or development for commercial purposes and for purchases of land or buildings for new residential development.

The investment zones will be developed alongside the existing freeports programme.

Infrastructure planning reform

The Planning and Infrastructure Bill will accelerate major infrastructure projects across England by streamlining the regulatory and consent processes involved.

The Government will work with the devolved administrations in relation to devolved planning responsibilities.

Pensions cap charge

Regulations will be introduced to remove ‘well-designed performance fees’ from the occupational defined contribution pension charge cap.

VAT-free shopping

A new shopping scheme free from any value added tax (VAT) will be developed for overseas visitors to Great Britain. This will enable them to obtain a VAT refund on goods bought in the high street, airports and other departure points and exported from the UK in their personal baggage. A consultation will gather views on the approach and design of the scheme, to be delivered as soon as possible.

Childcare reform

The Government has promised to bring forward reforms to improve access to affordable and flexible childcare.

Universal Credit

From January 2023, the administrative earnings threshold (AET) will increase to 15 hours a week at national living wage (£9.50 an hour) for an individual claimant and 24 hours a week for couples. This follows on from the increase to 12 hours for individuals and 19 hours for couples coming into effect from 26 September 2022.

Alongside the changes to the AET, the sanctions regime will be strengthened to set clear work expectations. Claimants could have their benefits reduced if they do not fulfil their job-search commitment without good reason.

Work coach support for over 50s

Additional work coach support will be provided to new eligible over 50s claimants and – for the first time – to over 50s who are long-term unemployed.

The Government will work with the Northern Ireland Civil Service to determine the most suitable arrangements for Northern Ireland in due course.

The Energy Price Schemes

By the time the Chancellor spoke, the Government had already announced two separate schemes aimed at limiting the impact of soaring gas and electricity prices.

The domestic energy scheme

The Prime Minister set out a range of measures on 8 September to protect domestic consumers from the £3,549 Ofgem utility price cap originally due to take effect for three months from 1 October:

- The key element was the EPG, superseding the Ofgem cap, set at an annual rate of £2,500 for two years from 1 October 2022. This will apply on the same basis as the Ofgem cap, i.e. a set of limits on standing and unit charges (see below) not on total bills.

- Customers with existing fixed-rate tariffs above the EPG level will generally see their standing and unit charges brought in line with the EPG, subject to a maximum subsidy of 17p/kWh for electricity and 4.2p/kWh for gas.

- The £400 flat-rate payment spread over six months announced in May will remain in place. The effect of this is to reduce bills by:

- £66 a month between October and December 2022; and

- £67 a month between January and March 2023.

- The other financial assistance announced in May, such as the £300 additional payment for pensioners, will also remain in place.

- There will be discretionary payments of £100 for those households using heating oil and liquefied petroleum gas (LPG).

- The same level of support will be given to households in Northern Ireland that are not subject to the Ofgem price cap.

The non-domestic energy scheme

On 21 September, the Department for Business, Energy and Industrial Strategy (BEIS) revealed details of its Energy Bill Relief Scheme (EBRS) for businesses, public bodies, charities and other non-domestic energy users.

The scheme applies to non-domestic customers who are:

- on existing fixed price contracts that were agreed on or after 1 April 2022;

- signing new fixed price contracts;

- on deemed / out of contract or variable tariffs; or

- on flexible purchase or similar contracts.

The EBRS will operate by reducing the estimated wholesale element of unit prices to Government supported price levels, subject to a maximum discount per unit.

For comparison, the BEIS estimates that the wholesale costs in England, Scotland and Wales for this winter are currently expected to be around 60p/kWh for electricity and 18p/kWh for gas.

Further details about the EBRS include:

- The EBRS support will apply for all eligible non-domestic customers for six months from 1 October 2022.

- The Government will publish a review in three months’ time focused on ‘the most vulnerable non-domestic customers’. This will form the basis for decisions about ongoing support after the EBRS ends.

- Equivalent support to the EBRS will be provided for non-domestic consumers who use heating oil or alternative fuels instead of gas.

- A parallel scheme to the EBRS, based on the same criteria and offering comparable support, will be established in Northern Ireland.

@ Copyright 23 September 2022. All rights reserved. This summary has been prepared very rapidly and is for general information only. You are recommended to seek competent professional advice before taking or refraining from taking action on the basis of the contents of this publication. The guide represents our understanding of the law and HM Revenue & Customs practice as at 23 September 2022, which are subject to change.